Jarvis™ Newsletter: Earnings in Full Swing: Shopify, Enphase, and More

Jarvis™ Newsletter: Earnings in Full Swing: Shopify, Enphase, and More

-Brian Dress, CFA, Director of Research, Investment Advisor

Overview:

We have mentioned in this newsletter ad nauseum that earnings reports are the key inputs to our fundamental investing process. This week we see earnings season in full swing, with many of the most important tech firms (among others) reporting their results. Such mega-cap companies as Apple (AAPL), Facebook (FB), Amazon (AMZN), and Microsoft (MSFT) reported earnings this week, but they have been covered extensively in financial media. In today’s newsletter, we will cover the earnings of three interesting companies that receive less media coverage: solar microinverter producer Enphase Energy (ENPH), e-commerce platform operator Shopify (SHOP), and oil refiner PBF Holdings (PBF), a name which we are following not for the common stock, but for the 7.25% 2025 bond.

Speaking of bonds, we want to remind you of our upcoming free webinar event “Fortune Makers: Income Securities” that takes place on Sunday, November 7, at 4pm Eastern/3pm Central. As investment professionals engaged in portfolio management, we know how difficult it is to find suitable income investments in the current low interest rate environment. In the Zoom event, we will cover our philosophy on selecting income securities like high yield bonds, preferred shares, and dividend paying stocks. We will also detail two actionable investment ideas and attendees will receive our new e-Book on income securities. Head over to our Eventbrite page to reserve your place in the webinar!

This week we saw a continuation of the momentum we have seen throughout the month of October: in the period covered in this letter (October 22-28), the S&P 500 gained 1.03%, the NASDAQ index advanced by 1.53%, but small caps continued to lag with the Russell 2000 flat on the week. Investors that remained steadfast in their optimistic view in September have seen the rewards of that patience in the month of October. Market reversals like the one we have seen in October are why we are so adamant that investors should avoid trying to time markets: buying back in after selling stock can be very difficult!

We have a special introductory offer to our LBIR subscription service for loyal readers of our newsletter. Please read to the end of this week’s review to find your coupon code to access our service for a 30-day low-cost trial offer!

If you like what you see here, please share this newsletter with other investors, friends, and colleagues. The success of the Jarvis newsletter depends on your word-of-mouth recommendation to other like-minded investors. Just in case you are not receiving the newsletter into your inbox on Saturday mornings, make sure to visit our website to get yourself on the mailing list. The Jarvis Newsletter is a great way to get your weekend started, as you use your time with the markets closed to do deeper research and prepare for the next week of investing.

Thank you, again, for your support in the early days of the Jarvis newsletter!

With that all being said, let’s get into it!

Interpreting the Jarvis Data (week of 10/22-10/28):

Best/Worst Performing:

Best/Worst Performing is a list driven by technical factors, like relative strength and stock price relative to moving averages. To learn more about how we use the “Best/Worst Performing” lists and the criteria Jarvis uses to choose stocks for each list, visit our Jarvis page and read the section entitled “Interpreting the Jarvis Outputs.”

Some weeks the Jarvis Outputs give us greater insights than others. We have seen some upheaval throughout the month of October, with some leaders of 2021 pulling back slightly and laggards, like technology specifically, coming back into favor. Because of this, we saw a relatively small number of stocks on the Best and Worst Performing lists this week and a record number of new entrants (since we have been writing the newsletter) to the “New Jarvis Ranks Under 50” list.

In last week’s letter, we shared with you that the Best/Worst ratio indicator continued to show positive momentum in markets, as the Jarvis output showed us a 24 to 9 Best/Worst Ratio. This week we saw a slight pullback in crude oil prices, which interrupted the momentum in the oil/gas space. Thus, many of the energy names dropped out of the Best Performing list. This week we saw a neutral ratio of 9 Best Performing stocks versus 9 stocks on the Worst Performing list.

Repeat readers know that we track which stocks from the “Best Performing” list appear for multiple weeks in a row, as we consider this a good indicator of short-term momentum. Of the 9 stocks on the Best Performing list, 6 were repeat entries, including Molina Healthcare (MOH), pipeline operator EnLink Midstream (ENLC), chipmaker Advanced Micro Devices (AMD), and solar power company SunPower (SPWR). Notable new entries to the list included customer relationship management software developer HubSpot (HUBS) and worldwide insurance carrier Chubb (CB).

Yet again, Worst Performing continues to favor small/mid cap companies, with six of the nine companies on this week’s list carrying an enterprise value below $8 billion. We had three companies that we follow closely come to the list this week: Teva Pharmaceuticals (TEVA), cloud communications software company Twilio (TWLO), and online brokerage Robinhood Markets (HOOD).

Left Brain•Logic Many of the dramatic moves this week were earnings related: AMD reported impressive earnings, in which management discussed how the business continues to take share away from Intel (INTC). On the other side of the ledger, TWLO and HOOD had earnings reports that investors did not look upon favorably.

We have long been admirers of AMD and their superstar CEO Lisa Su, so that result was not surprising. We were slightly surprised at the TWLO miss, but we are still bullish on the long-term prospects for the company. HOOD’s earnings told a story that revenues fell sharply as volumes for Dogecoin dropped precipitously. We are not bulls on HOOD, especially considering that the company’s revenues are so dependent on trading of meme stocks and coins.

New Ranks Under 50:

“New Ranks Under 50” is one of our favorite features in the Jarvis system. We use the feature to identify stocks with clear upward momentum. We have not written this section over the past few weeks, as there were more interesting topics to discuss, but we are bringing it back for this week due to the large turnover in our top 50: we saw a record (since we have written the newsletter) of 12 new names in the Jarvis Top 50.

Among the new entrants to the top 50 were a couple of our old favorites that spent many weeks on the Best Performing list in August/September: purveyor of rubber clogs Crocs (CROX) and diabetes device maker DexCom (DXCM). A good number of new entrants were earnings stories, including Microsoft (MSFT), oil/gas producer SM Energy (SM), and Enphase Energy (ENPH), a name we will discuss in more depth below. Other stocks that showed continued momentum from positive earnings reports last week were Tesla (TSLA) and asset manager Blackstone Group (BX). Finally, the list is rounded out by other energy stocks in Petroleo Brasileiro (PBR) and Imperial Oil (IMO).

Left Brain Logic It is not terribly surprising to see turnover, given this week’s barrage of earnings. Energy continues to be one of the biggest drivers in the markets. SM, PBR, IMO, and SM are direct beneficiaries of the trend, while stocks related to alternative energy like TSLA and ENPH are seeing momentum as an indirect result.

It’s been a while since we saw our old favorite CROX on any of our Jarvis lists, but we have not changed our view that this is a very well-run retailer with a bright future. We also remain bullish on BX and DXCM.

ETF List -- Most Risen/Dropped:

The ETF List is the way we follow sector trends. In Jarvis, we rank roughly 300 ETFs on a weekly basis and track which of these rose and dropped the most over the past week. Though we focus more on the micro than the macro, it is important to recognize which sectors are strongest at any given time, to help us identify opportunities that exist in our blind spots.

· ETF List - Most Risen: As we referenced above with the inclusion on SPWR and ENPH in various Jarvis output lists, the solar industry was strong over the past week, with Invesco Solar ETF (TAN) the strongest ETF for the week up 8.73%, followed closely by the iShares Global Clean Energy ETF (ICLN). Notable also was the continued strength in the Crypto space, with the Grayscale Ethereum Trust (ETH) and Bitwise Crypto Industry Innovators ETF (BITQ) both among the top 5 performing ETFs in our list.

We have been covering natural gas in the newsletter relentlessly over the past two months. After a down week last week, the United States Natural Gas Fund, LP (UNG) recovered sharply this week, up 6.17%.

Momentum continues in the growth stock/tech space, with the SPDR S&P Semiconductor ETF (XSD) and Invesco S&P 500 Pure Growth ETF (RPG) repeat entrants to this week’s list. We see another interesting repeat entrant in Invesco Global Listed Private Equity ETF (PSP), reflecting investor interest in gaining exposure to private equity deals. A new entrant to our list was Consumer Discretionary Select Sector SPDR Fund (XLY).

Treasuries were strong this week, as the ten-year US Treasury rates slipped back below 1.6%. Among the top performing ETFs in fixed income were PIMCO 25+ Year Zero Coupon U.S. Treasury Index Exchange-Traded Fund (ZROZ) and iShares 20+ Year Treasury Bond ETF (TLT).

ETF List - Most Dropped: The most dropped list was all over the map. Of course, vehicles that represent bearish bias on US Treasuries suffered, including ProShares UltraShort 20+ Year Treasury (TBT). Cannabis stocks were among the weakest of any sector we cover, represented by the 7.36% pullback in AdvisorShares Pure US Cannabis ETF (MSOS). Aerospace/defense was also weak, as represented by Invesco Aerospace & Defense ETF (PPA).

Municipal bonds continued their slide, with Pimco Municipal Income Fund III (PMX) a repeat entrant to the Most Dropped list.

We again saw weakness in China, as KraneShares CSI China Internet ETF (KWEB), iShares MSCI China ETF (MCHI), and iShares China Large-Cap ETF (FXI) all made the Most Dropped list.

In the commodity space, we saw weakness in iPath Series B Bloomberg Copper Subindex Total Return ETN (JJC) and ClearBridge MLP and Midstream Fund Inc (CEM).

Left Brain Logic We have noted strength in the alternative energy space over the past few weeks, finally seeming to catch up with the fact that oil prices have been elevated for a long time. The longer oil remains elevated, the better for these stocks, like ENPH.

Growth stocks and crypto strength are major themes for the second week in a row. We will be watching closely next week to see if this continues and whether the last two months of 2021 will be favorable for these two sectors.

It is interesting that Muni Bonds have continued their decline, even as treasury rates come down. We think the risk/reward is not in the favor of investors in munis and caution should be exercised.

Cannabis continues to be one of the worst performing sectors anywhere, as does anything related to China. We remain bears on both cannabis investing and China.

Finally, we note that copper has dropped more than 10% in the last 10 days of trading. This, coupled with the rise in US Treasuries, could be an indicator that inflation fears are abating. We will continue monitoring these two key indicators of inflation in the context of the relentless inflation narrative.

Earnings Reviews from This Week

We saw a barrage of earnings this week, including from mega-cap tech names like Facebook (FB), Microsoft (MSFT), Amazon (AMZN), and Apple (AAPL). Those have been covered extensively by financial media, so we will leave you to read about those elsewhere. Aside from the names we are writing up below, we saw market moving earnings reports from Twilio (TWLO), ServiceNow (NOW), Snap Inc. (SNAP), Teladoc Health (TDOC), and many more. We have chosen three reports below that were of interest to our eye and our fundamental analysis process.

Enphase Energy (ENPH)

Enphase Energy was one of the best performing stocks of 2020, advancing by more than 400% in that calendar year. The stock fell out of favor in early 2021, with a closing low of 114.61 on May 13. Since then, the stock has doubled, buoyed particularly by the most recent earnings report on Tuesday, since which the stock has rallied some 30%.

ENPH is one of the premier players in the solar industry. The company produces microinverters, which allow users to convert direct current (DC) provided by solar panels into usable alternating current (AC), which is the protocol of household and commercial electronics. The company has also expanded into battery and storage technology, as well as a software system that manages the entire system. As we mentioned above, solar businesses like this traditionally do well in times of high oil prices. We sat waiting for ENPH to follow that pattern throughout 2021, but the stock has only just started to move, from 145.03/share on October 4 to the October closing price of 224.26.

Investors were especially excited about the company’s Q3 earnings, which were released on Tuesday of this week. For the quarter, the company delivered a record revenue print of $351.5 million, which represents an astonishing 97% annual growth rate over the same quarter last year. Gross margins came in at 41% (of revenue), with operating expenses at 16% of revenue and operating profit of 24%, all of which compare favorably to the company’s overall baseline goal of 35/15/20, respectively. These profit figures were impressive in the context of the cost inflation we have seen throughout the economy, during the period. Management stated that the company plans to push through a single-digit price increase in the 4th quarter to cope with the cost pressures associated with supply chain issues.

In the quarter, ENPH was able to ship some 2.6 million microinverters and is making great progress toward its goal of capacity to produce 5 million per quarter by year end. At present, quarterly capacity between its manufacturing facilities in Mexico and India stand at a combined 3.7 million per quarter.

Demand appears to be strong for Enphase’s suite of products, between its microinverters, batteries, and software. Supply of microchips has been a challenge for production, but Q4 should be better than Q3 in this regard. There have also been delays due to shipping constraints, but the company expects this condition to work itself out over the coming quarters. Said CEO Badri Kothandaraman “We are optimistic that our supply will catch up to demand by early next year.” Enphase has shipped some microinverters via air, but the size of the storage systems precludes this workaround for that segment of the business.

There is plenty of interest on the horizon for ENPH. The company is getting ready to ship its IQ8 microinverter product, that will be the first product that can provide dedicated backup power during a power outage without a battery attached. Customers that purchase an IQ8 and a battery system will be fully energy independent and even can sell power back to the grid in select geographies, including New England and Hawaii.

For Q4, management expects revenue of $390-410 million, which at the midpoint implies a growth rate of 52% over Q4 2020. There are limited issues of supply due to manufacturing, rather shipping and logistics remain the major impediment to decreasing the current 14-week lead time to deliver product. Because of the uncertainty around shipping, management declined to give guidance for 2022.

All in all, we were impressed by the report and we remain constructive on Enphase going into 2022. The company is a clear leader in its field and has continued to deliver on lofty growth expectations. This is certainly a Left Brain type of stock.

Shopify (SHOP)

Shopify has been one of the best performing stocks over the past five years, delivering more than 8500% return to investors since the May 2015 IPO. This has been a stock that has been hard to purchase since it always appears expensive. However, SHOP is a case in point why a high valuation is not a sufficient reason to sell or avoid buying a stock.

Shopify operates an e-commerce platform that empowers businesses of all sizes to sell their products online and, increasingly, is facilitating omnichannel sales strategies of large brick-and-mortar enterprises. The gross merchandise value (GMV) sold on the platform has impressively doubled from $200 billion to $400 billion in just the last 16 months. Certainly, SHOP was a key beneficiary of the pandemic, but this explosive growth of the platform is also a testament to the company’s supreme execution. CEO Tobi Lutke is one of the highest-ranked CEOs we have studied in our CEO Profile series.

After the report’s release before market open on Thursday, investors initially sold the stock aggressively in pre-market. However, after more information was released, price action reversed and shares ended up more than 7% for the day. Third quarter revenue came in just below consensus expectations at $1.1 billion (implying 46% Year-over-Year growth), which is rather high considering the 86% growth announced in the same quarter in 2020. Management shared that revenue was lower than expected, due to the supply chain issues faced by some of its merchants and as stimulus funds in the US dissipated. With that said, management reiterated full year guidance for 2021 will be in line with projections made back in February.

Shopify is aggressively expanding the services it offers to merchants, as well as its integrations with outside applications. Shopify Payments has been shown to boost repeat purchases among first time buyers by 23%, which is a strong value proposition for merchants. In Q3, Shopify Payments grew by 49% on an annual basis and now accounts for nearly half of the transactions that take place on the overall Shopify platform. Additionally, innovations include new integrations with TikTok and Spotify, as well as a Point-of-Sale software system that merchants can use in their brick-and-mortar locations. Finally, CEO Lutke noted that thousands more merchants are taking advantage of the existing integrations with Facebook, Instagram, and Google.

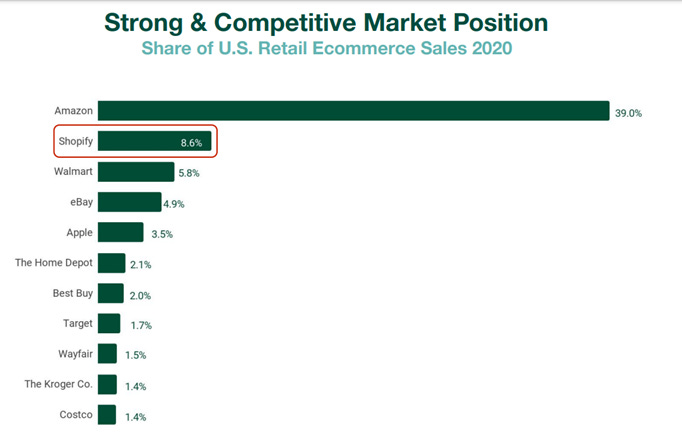

Shopify continues to build on its market position. Certainly, Amazon continues to dominate e-commerce, but as you can see in the slide below, Shopify is a solid #2 in this space. For the quarter, Shopify had a number of exciting customer wins, including Spanx, Logitech, Tupperware, FTD Florists, and Jennifer Aniston’s new beauty brand.

With respect to supply chain concerns that are dogging businesses of all stripes, Shopify has not been immune. However, despite these challenges, Shopify is moving forward with previous guidance. Management noted that merchants have been using the Shopify’s software and services suite has helped position merchants to cope with inflationary pressures and supply chain issues.

We continue to be impressed with the growth and execution associated with Shopify. Nothing in the past quarter’s results changes our view and we remain bullish on SHOP shares.

PBF Energy (PBF)

PBF Energy is a petroleum refiner with five facilities scattered across the US. We have been following this company for most of 2021, not for investment in the common stock, but rather looking closely at the 7.25% 2025 bond, which is a high yield issue. To give you a bit of background of how we approach bond investing differently than stock investing: for bonds, we are looking for stability in the company’s balance sheet, its plans for deleveraging, access to capital markets, and the trajectory of cash flows. We are less concerned with revenue growth rates, as we would be when we are assessing a common stock opportunity.

As you can see in the chart below from FINRA Trace, the 2025 PBF bonds have had a wild ride in 2021. In July of this year, the bonds sold off precipitously on a less than stellar Q2 earnings report. The major challenge the company faces comes from the so-called RIN credits, which the US government forces refiners to purchase to offset the environmental impact of their production. Because of the scarcity of these credits, the prices of RINs have exploded in recent years, putting heavy pressure on the company’s profitability.

Because gasoline demand has increased in the US through Summer 2021 and beyond, refining margins have improved. According to management, demand for diesel fuel is now back above pre-COVID levels, while gasoline demand is at parity with 2019 levels. It is good to see that the business is improving. As a result, PBF was able to deliver positive free cash flow over and above its fixed costs for the first time since the pandemic hit.

As we stated above, we are most interested in how these improvements are impacting PBF’s balance sheet, as we assess the creditworthiness of the company. In Q3, PBF was able to purchase $229 million of outstanding bonds in the open market, at an average price of 64 cents on the dollar. This brings the total of bond retirements to $300 million for 2021 and the company boasts $1.4 billion in cash on hand. Since PBF carries roughly $4.5 billion in outstanding debt, net debt stands at around $3 billion. In other words, PBF has paid off 10% of its net debt in 2021 and plans to continue to do so. PBF’s total liquidity is $2.6 billion ($1.4 billion cash + $1.2 billion in credit capacity). Management says PBF only needs $900 million in liquidity to operate the business efficiently, so the cash on the balance sheet is a potential lever to pull, as the company continues to deleverage the business.

As regards PBF, we see marked improvement both in the business and in the fiscal situation here. The 2025 bonds currently carry an annual yield of about 14.7%, so the opportunity is fairly attractive for income investors willing to bear a bit of risk. Given the fiscal and business trajectories in play here at PBF, we think the risk/reward is favorable for bond investors.

Earnings Preview for Next Week

We spoke two weeks ago about our method for digesting earnings calls and how that fits in with our investment philosophy. We had a deluge of earnings this week from some of the largest and most important tech firms in the US, but there are plenty more earnings reports we will be watching next week:

· Etsy (ETSY) – Wednesday: Etsy is a platform where users can sell their artisan goods and crafts. This has been one of the strongest performers in the post-pandemic era and we are interested to see whether loosening of COVID restrictions has a negative impact on the company’s results.

· EPAM Systems (EPAM) – Thursday: EPAM has been a strong performing stock, especially when compared to other technology companies. The shares have nearly doubled year-to-date. EPAM does digital transformations for large enterprises. We will be interested in the effect of return to the office on the company’s strong business trajectory since the pandemic began.

· Mercado Libre (MELI) – Thursday: We wrote on October 1 that Mercado Libre was a stock whose share price was punished brutally in the tech selloff of September. We are long-term bullish on this company, which is a combination of an e-commerce platform in Latin America and a payments processing business (Mercado Pago). We are interested in learning more about how the Latin American economy is responding to the delta wave of COVID and whether the company can continue to deliver the type of explosive growth it has previously reported.

· Square (SQ) – Thursday: Square is one of the premier FinTech stocks anywhere in the world. The company has had great success with its point-of-sale systems used in many small businesses, but has also gained traction with the Cash App, a mobile payments processing system that is very popular. Note also that SQ has significant exposure to the crypto space, as the Cash App empowers users to buy and sell cryptocurrency with one click. We are interested in how the payments business is doing as a proxy for overall economic activity, as well as whether the rise in crypto prices over the last quarter has a material impact on results.

· Wynn Resorts (WYNN) – Thursday: Wynn operates casinos all over the world, including in Macau (China) and in the US. The stock has been under major pressure since the Chinese government imposed new restrictions on the casino business. We will be watching closely to see the level of impact the new rules in China have on overall results.

Takeaways from this Week

This week, the recovery in growth stocks continued again, as it has for most of October. Over the past month, there has been a fair bit of upheaval in which stocks lead and lag, as tech stocks have gained steam at the expense of cyclicals and other “reopen trades”.

We saw the biggest set of tech earnings this week and most of those reports were positive. In particular, we like the reports we read from ENPH and SHOP. We will be watching a number of key earnings reports next week to gain additional insights. Remember, this is the most important time for investors to learn about the stocks they own.

The energy sector was a mixed bag this week, as oil prices dropped slightly and natural gas prices rose significantly. We still like the sector as an investment opportunity and we think the PBF 7.25% 2025 Bonds offer an interesting risk/reward proposition.

Thanks again for your continued support of Left Brain and the Jarvis newsletter. Again, if you found value here, we would humbly ask that you pass the newsletter along to friends or colleagues with interest in investment strategy. Make sure you sign up to receive the newsletter weekly in your inbox, if you haven’t already. Have a great weekend and we will speak with you again soon!

Announcements:

(1) A special offer for readers of our Jarvis newsletter. For the next week, we are offering a 30-day trial of the Basic Subscription for just $99 (67% off the normal price). Just enter the coupon code ‘Spooky99’ at checkout. Note that the fee will go back to normal price after the initial 30 days.

(2) We are just 9 days out from the next installment of our Fortune Makers webinar series. On Sunday, November 7 at 4 pm Eastern/3pm Central, we will host our free webinar on Income Securities. Our investment team will speak briefly on the role of income securities in a balanced portfolio, while also providing you two actionable ideas for investors looking for sources of income in their holdings. Please visit our Eventbrite page for details on how you can sign up for the event. Note also that attendees will receive our e-Book which details the way Left Brain looks at income securities, including bonds, preferred stocks, high dividend stocks and more!

(3) Don’t forget to sign up to receive the Jarvis newsletter in your email inbox every week. Make sure to check your spam/promotions folders if you don’t receive it after signup.

(4) We hope the insights of the Jarvis newsletter are helpful to you as you get ready for the next week of stock market action. Please share this newsletter with your network if you found it of use. That’s the best way for our work to be found! For more details on Left Brain, Jarvis™, or anything else investing related, please reach out to us at www.LeftBrainIR.com. Feel free to contact me directly at briand@leftbrainwm.com or at (630) 547-3316 with any questions. We would love to receive your reader feedback on how we can make this weekly letter more useful to you, as you manage your portfolio and/or choose an advisor to help you accomplish the task.

(5) With the markets showing increased volatility over the past few months, we know that many investors are wondering if they need a “second opinion” on their investment positioning, whether they manage their own money or use an advisor. We stand ready and willing to help and we are thus offering a complimentary portfolio review to interested investors. Just reach out to us on the link provided and we will contact you within a few days to help you assess whether your portfolio is well-positioned to take care of business and market trends!

Thank you and we wish for you another week of profitable investing. Enjoy the weekend!

DISCLAIMER: This report contains views and opinions which, by their very nature, are subject to uncertainty and involve inherent risks. Predictions or forecasts, described or implied, may prove to be wrong and are subject to change without notice. All expressions of opinion included herein are subject to change without notice. Predictions or forecasts described or implied are forward-looking statements based on certain assumptions which may prove to be wrong and/or other events which were not taken into account may occur. Any predictions, forecasts, outlooks, opinions or assumptions should not be construed to be indicative of the actual events which will occur. Investing involves risk, including the possible loss of principal. The opinions and data in this report have been obtained from sources believed to be reliable; neither Left Brain nor its affiliates warrant the accuracy or completeness of such, and accept no liability for any direct or consequential losses arising from its use. In addition, please note that Left Brain, including its principals, employees, agents, affiliates and advisory clients, may have positions in one or more of the securities discussed in this communication. Please note that Left Brain, including its principals, employees, agents, affiliates and advisory clients may take positions or effect transactions contrary to the views expressed in this communication based upon individual or firm circumstances. Any decision to effect transactions in the securities discussed within this communication should be balanced against the potential conflict of interest that Left Brain, its principals, employees, agents, affiliates and advisory clients has by virtue of its investment in one or more of these securities.

Past performance is not indicative of future performance. The price of securities can and will fluctuate, and any individual security may become worthless. A high or favorable rating, rating outlook, gauge, or similar opinion is not indicative of future performance, and no user should rely on any such rating, rating outlook, gauge, or similar opinion to predict performance or potential for return. Future performance may not equal projected or forecasted performance or potential for return. All ratings and related analysis, as well as data, statistics, analysis and opinions contained herein are solely statements of opinion and are not statements of fact or recommendations to purchase, hold, or sell any security or make any other investment decisions.

This report may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will materialize. Reliance upon information herein is at the sole discretion of the reader.

THE REPORT IS PROVIDED ON AN "AS IS" AND "AS AVAILABLE" BASIS WITHOUT REPRESENTATION OR WARRANTY OF ANY KIND. Left Brain Investment Research LLC DISCLAIMS ALL EXPRESS AND IMPLIED WARRANTIES WITH RESPECT TO THE REPORT, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

The Report is current only as of the date set forth herein. Left Brain Investment Research LLC (LBIR) has no obligation to update the Report or any material or content set forth herein.

LBIR is an affiliate of Left Brain Wealth Management LLC, an investment advisor registered with the Securities and Exchange Commission. LBIR is an affiliate of Left Brain Capital Appreciation Fund, L.P., Left Brain Capital Appreciation Offshore Ltd, and Left Brain Capital Appreciation Master Fund, Ltd., all of which are hedge funds managed by Left Brain Capital Management, LLC. The general partner of these hedge funds, Left Brain Capital Management, LLC, is an affiliate of LBIR.

© 2021, Left Brain Investment Research LLC. All rights reserved. Reproduction in any form is prohibited.